I am your Wisconsin home loan specialist for life, NMLS #278204 and I work for Inlanta Mortgage, Brookfield WI. I offer all types of lending products from conventional, FHA, 203k, VA, USDA and more. I also offer first time home buyer seminars and well as credit guidance for those that may have had some credit troubles in the past. Buying or refinancing, I want to be your, as well as your friends and families, home loan specialist for life. Contact me for all of your home loan needs.

This blog post was inspired by a mistake made while cooking dinner. Over cooking food is wasteful on more than one level. This short video explains how simply setting a timer will save you money. (Click play or read the text from the video below). Enjoy and if you or anyone you know needs help saving money on their mortgage or needs help getting qualified for a home purchase loan please call me.

This installment of the Money Saving Minute brought to you by

This is a cooking timer this is not

Money Saving Minute number zero one zero - set your timer. Like most people, my time is limited so I have a tendency to try and tackle several tasks at once. In my haste to get both dinner cooked and laundry done I neglected to set my cooking timer. While I was gnawing threw my shoe leather chicken it occurred to me that overcooking is wasteful on more than one level. First, overcooking leads to food waste. If its dry or burnt chances are the leftovers are going in the garbage . . . If not the entire dish. Second, overcooked food requires something to help make it palatable so most of us reach for Catsup, butter or some kind of sauce. These condiments add unwanted calories and expense to a meal. Finally, although it may only be pennies, over cooking food requires more energy than food cooked to the correct doneness. So, by simply setting a timer when cooking we waste less food, don’t use as much high calorie condiments, save on energy and have a meal worth eating. This has been money saving minute number zero one zero. It’s your cash and watching The Money Saving Minute each week will help you keep more of it. Click to the right to subscribe so you don’t miss any money saving tips and click the facebook button below to share this with your friends.

Each person potentially has three credit scores.

Each score is based

on five factors and each of

these factors is weighed differently.

Click

play to learn more or read the text from this video below.

As a mortgage banker I deal with

credit on a daily basis. If you have questions about any of the information

presented in this video I am available by phone or email.

Money Saving Minute number 010

- How are credit scores calculated?

When credit is run, the three most

common questions are: What are my scores, are those scores good or bad and how

is that number calculated?

Credit Scores are calculated from

several different pieces of credit information. This data is grouped into five

categories. Each category is weighed differently and is expressed in the form of

a percentage. Your score considers both positive and negative information in

your credit report. Late payments will lower your FICO Score, however

establishing or re-establishing a good track record of making payments on time

will raise your score. These percentages are based on the importance of the

five categories for the general population. Every individual's situation is

weighed slightly differently. In other words, this is the guideline, not the

rule.

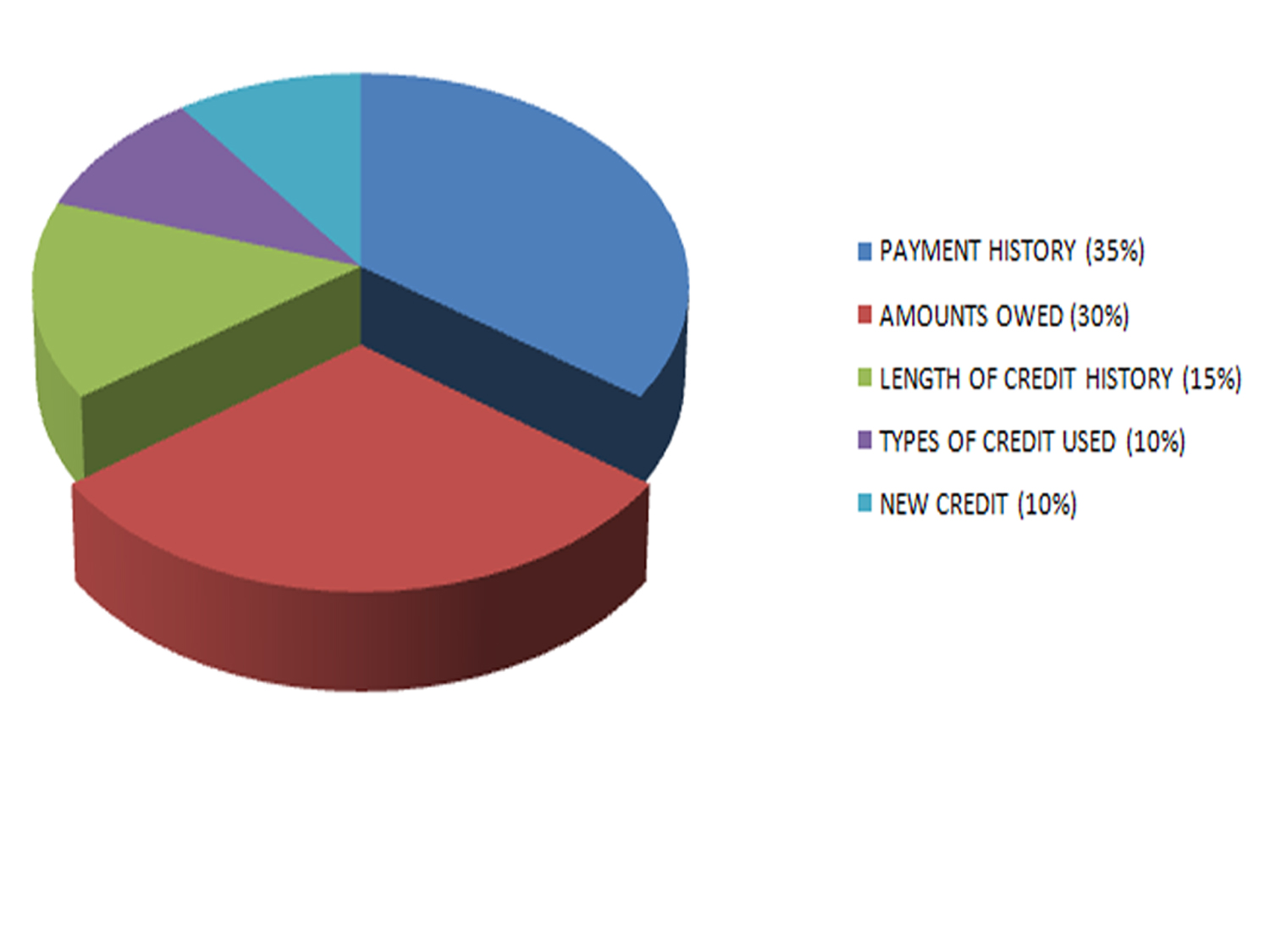

35% PAYMENT HISTORY 30% AMOUNTS

OWED 15% LENGTH OF CREDIT HISTORY 10% TYPES OF CREDIT USED 10% NEW

CREDIT

Payment

history (35%) This is the most important factors in your credit

scoring. A few late payments can have a large impact on your score if you have

limited credit. The more trade lines that you have in good standings will

determine on how quickly you will earn those points back. Please note, however,

having no late payments in your credit report doesn't mean you’ll have perfect

credit. Your payment history is just one of the five factors in calculating

your credit Scores.

Amounts owed

(30%) Owing money on credit accounts doesn't necessarily mean you're a

high-risk borrower. However, when a high percentage of a person's available

credit is been used, this raises the risk level for a lender and therefore

lowers the credit score. Note that even if you pay off your credit cards in

full each month, your credit report may show a balance on those cards. The total

balance on your last statement is generally the amount that will show in your

credit report. In addition to the overall amount you owe, your FICO Score

considers the amount you own on specific types of accounts, such as credit cards

and installment loans. Carrying a very small balance without missing a payment

shows that you managed credit responsibly and having a low credit utilization

ratio is a plus for your credit scores. But you need to have to have credit in

order to have a score. The misnomer that by paying cash for everything means

that you have great credit is false. Cash is king but it doesn’t buy you 700

scores. Also, closing unused credit accounts that have zero balances and are

in good standing will not raise your scores. As a matter of fact, they may

actually lower you scores because you are reducing your utilization ratio. If

an unused account is costing you money in annual fees, however, than closing the

account should be something to consider but only if you have other accounts

reporting favorably for you.

Length of

credit history (15%) In general, a longer credit history will increase

your credit scores. However, even people who haven't been using credit long may

have good credit scores, depending on how the rest of the credit report

looks. Your FICO Score takes into account how long your credit accounts have

been established, including the age of your oldest account, the age of your

newest account and an average age of all your accounts. Scoring also considers

how long specific credit accounts have been established and how long it has

been since you used certain accounts. This plus utilization ratio are why short

term loans do not help to reestablish credit bad credit. A high interest twelve

month loan from a store might get you a new TV but it's not going to get you

into a higher credit rating. Reestablishing credit takes time and the proper

tools.

Types of

credit in use (10%) Scoring will consider your mix of credit cards,

retail accounts, installment loans, finance company accounts, utilities and

mortgage loans. The credit mix usually won’t be a key factor in determining

your FICO Score but it will be more important if your credit report does not

have a lot of other information on which to base a score.

New credit

(10%) Opening several credit accounts in a short period of time

represents a greater risk - especially for people who don't have a long credit

history. Also, reaching the maximum level on a new account as soon as you open

the account can have a negative impact. If you are taking out a line of credit

for a specific purchase, such as a new washer and dryer, request a limit that is

higher than your purchase. Even if you are planning on paying off the purchase

within a short period of time the account will always show that the limit and

the historic high balance are the same.

Importance of

categories varies per person The importance of any one factor in your

credit score calculation depends on the overall information in your credit

report. For some people, one factor may have a larger impact than it would for

someone with a much different credit history. In addition, as the information in

your credit report changes, so does the importance of your other factors in

determining your scores. Use these ratios as a guide to build a healthy credit

profile as well as a planning tool when making credit related

decisions.

This has been money saving minute

number zero zero nine. It’s your cash and watching the The Money Saving Minute

each week will help you keep more of it. Click to the right to subscribe so you

don’t miss any money saving tips and click the facebook button below to share

this with your friends.

Even energy efficient bulbs still require energy to work and leaving lights on in unoccupied rooms has a direct link to your energy bill. Click play to learn more or read the text from the video below. If you find this information useful please feel free to share this with your facebook and G+ friends. And if you know anyone that needs help with their current mortgage or help getting qualified to purchase a home please call me.

Money Saving Minute #008: Turn Off The Lights (text from video)

This weeks tip is one that we all know because we have been told from the day we could reach the light switch to turn off the lights when we leave a room. So why don’t we? Old habits? Myths about using more energy to turn the light back on? Or is it that we don’t see the relationship between flipping a switch and our checkbook? The amount of money can you save by turning off lights is determined on how many lights you have running, at what power rating and for what amount of time. For instance if you have one light bulb with a 30 watt rating running for 100 hours that will be 30kW-hours. If your electricity is being supplied at $0.18/ kW-hour then 30 kW-hours is equal to $5.40. With numerous lights, turning them off can offer a real saving over a long period of time, not to mention an important environmental benefit. But doesn’t it take more energy to turn a light on and warm up the bulb than it does to just leave it on? Well, according to Mythbusters (video). This has been money saving minute number 007 - It’s your cash and watching the The Money Saving Minute each week will help you keep more of it. Click to the right to subscribe so you don’t miss any money saving tips and click the facebook button below to share this with your friends.